There’s nothing quite like the calm before a financial storm—your budget looks stable, salary has landed, things are finally aligning… then boom! A surprise electricity bill, an emergency trip to your hometown, your generator packs up, or your child’s school sends a sudden payment reminder. If it’s not one thing, it’s another. And just like that, your perfectly planned month unravels.

If you’re Nigerian, you already know—“emergency” is almost a financial category of its own. And whether it hits at the end of the month or five days after payday, unexpected bills have a way of throwing everything off balance. The anxiety kicks in, you start doing mental gymnastics, checking your balance more times than necessary, and asking yourself: “How did I not plan for this?”

This article isn’t here to judge. It’s here to help. Think of it as your financial first aid kit—a calm, practical guide to help you stop the spiral, breathe through the chaos, and find a way forward.

Take a Breath First – Don’t Panic

Before you start borrowing from Peter to pay Paul—or spiraling into worry—pause. Seriously. When unexpected bills land, our first instinct is often panic. But panicked decisions rarely lead to smart outcomes. You might think a quick loan or dipping into rent money is the only way out, but acting in urgency can deepen your money mess.

Instead, take stock. What’s the actual amount you need? Is it due right now, or is there wiggle room? Can you negotiate a payment plan, request an extension, or partially offset the bill in the meantime? You’d be surprised how much clarity a calm head can bring.

This initial step might not feel like action, but it’s the most important. By taking a breath and surveying the situation, you avoid the kind of knee-jerk responses that lead to more financial strain. Emergencies feel urgent—but clarity, not chaos, is your best starting point.

Read: What’s Your Money Personality? (And Why It Matters)

Re-Prioritize Your Budget Immediately

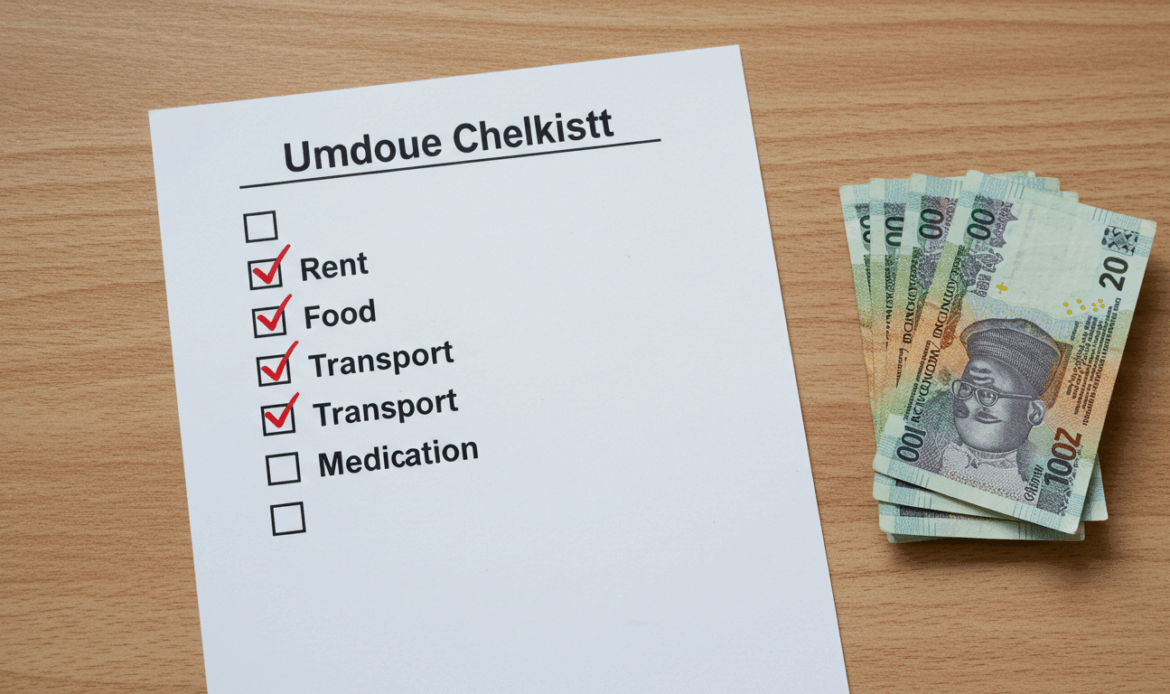

When life throws a financial curveball, your budget needs to go into emergency mode. Think of it like triage—what’s essential stays, what’s non-essential can wait. For most Nigerians, our monthly budgets are already tight, but there’s always room for short-term rearrangement when pressure hits.

Start by identifying your fixed essentials: rent, feeding, transportation, and key utilities. Then ask: what can be paused, reduced, or swapped? Maybe that data plan upgrade can wait, or you can switch from eating out to cooking at home. For the next few weeks, your spending should reflect one priority—clearing or managing that unexpected bill without spiraling into more debt.

You’re not failing if you shuffle things around. This is how financially resilient people operate—they adjust quickly, rather than allowing one expense to destabilize their entire financial situation. A short-term reset can prevent long-term consequences.

Explore Immediate Help—Without Shame

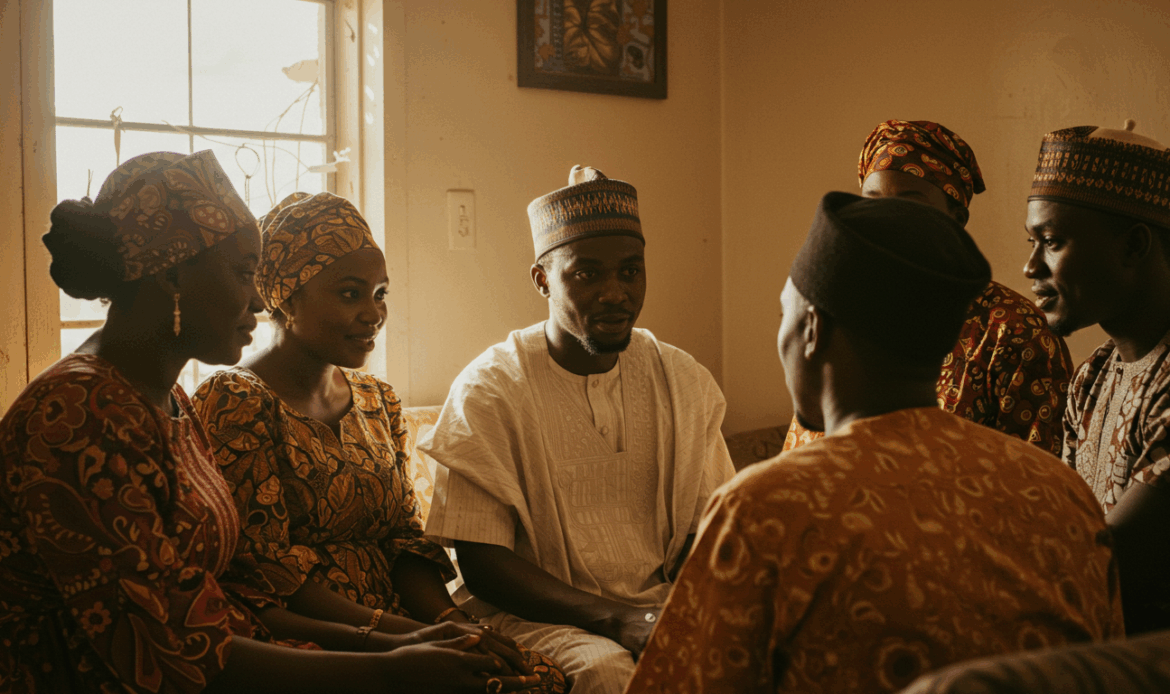

There’s a cultural weight to asking for help, especially when money’s involved. But if you’re hit with an unexpected bill—say, a medical emergency or a car repair—you shouldn’t let pride keep you from staying afloat.

Start with your personal network. This doesn’t mean mass-broadcasting your stress on social media. Instead, think about who in your circle you trust—friends, family, even faith-based or community groups. A short-term loan or assistance can often come with zero interest and more grace than any bank will ever offer.

For more structured help, explore financial institutions or fintech platforms that offer low-interest microloans. In Nigeria, platforms like Carbon, FairMoney, or even cooperative societies can bridge gaps. Just ensure you fully understand the repayment terms.

And if you need time to pay a bill—negotiate! Many service providers or landlords would rather hear from you than be ghosted. A payment plan is better than radio silence.

Asking for help isn’t weakness; it’s wisdom. It’s how you prevent a one-time problem from becoming a long-term crisis.

Read: How To Monetize What You Already Know

Cut Back Without Feeling Deprived

When financial surprises hit, your instinct might be to freeze all spending. But an all-or-nothing approach often leads to burnout—and ultimately, more impulse spending. Instead, go tactical.

Start with a spending audit. Review your expenses from the last two to four weeks and identify any leaks, such as recurring subscriptions, extra data purchases, or unplanned takeouts. Cancel, pause, or reduce where possible. Focus on trimming—not gutting—your lifestyle.

Then, redefine “treats.” Instead of a ₦15,000 dinner, host a potluck. Replace that ride-hailing bill with a bus ride or carpool. You’re not punishing yourself; you’re redirecting your money with intention.

Give every naira a purpose. Assign it toward food, utilities, transport, or savings. Create a mini cash envelope system, even digitally, to help stay in control.

Cutting back doesn’t mean living less. It means spending smartly and flexibly, without guilt or deprivation. Financial resilience isn’t about having more money—it’s about making better decisions with what you have.

Plan Your Recovery Strategy

Once the immediate storm passes, don’t just move on—learn from it. A recovery plan ensures that the next financial surprise doesn’t feel like an emergency.

Start with reflection. What caused the shortfall? Was it poor planning, delayed income, or an unexpected event, such as medical bills or home repairs? Clarity here helps you avoid repeating the cycle.

Next, rebuild your emergency buffer—slowly but intentionally. Even ₦2,000 a week adds up over time. Use automatic transfers or save loose change digitally. Make the fund visible and name it something empowering like “My Safety Net.”

Adjust your budget moving forward. Factor in mini-sinking funds for predictable but irregular expenses, such as school fees, car repairs, or holiday spending.

Lastly, have a money check-in every month. Make it as routine as laundry—review what went well, what slipped, and where to improve. Financial recovery isn’t a one-time fix; it’s a habit.

Because when you recover well, you build confidence. And that’s more valuable than a windfall.